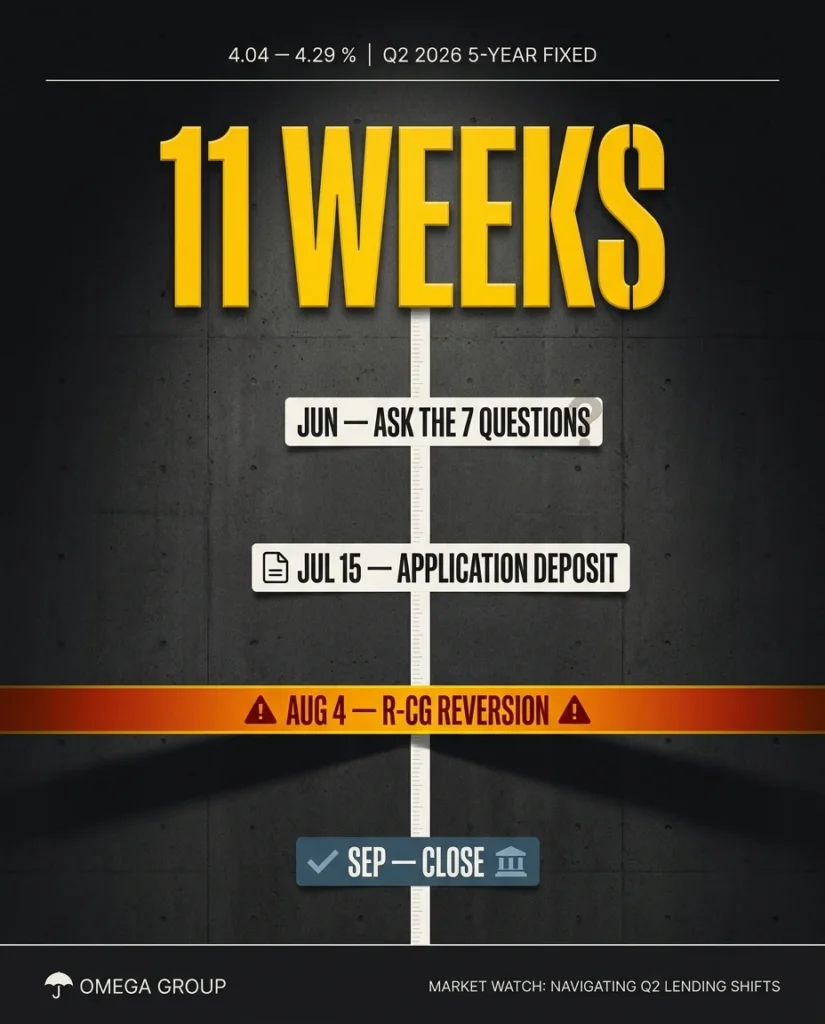

A Tuscany-edge GP in May 2026 has a 6-unit deal underwritten under MLI Select Tier 100. His lender pre-quoted 4.18% on a 5-year fixed. The April 8 R-CG vote landed; his April quote is now stale. The August 4 reversion is 11 weeks out. He’s about to submit the permit — and his lender hasn’t called.

This is the gap between a deal that closes in September and one that sits dead while the deposit burns. Q3 2026 in Calgary multi-family is not a normal quarter — the August 4, 2026 R-CG reversion is reshaping the as-of-right pipeline, CMHC’s February 2025 MLI Select clarification has narrowed several configurations that earlier underwriting accepted, and lenders’ underwriting committees are operating on calendars the GP does not control. The seven questions below are the ones that change whether the deal closes — or whether the GP is the last one to find out it didn’t.

1. Is my deal still MLI Select eligible after the latest CMHC rule reading?

A Mahogany-fringe GP was pre-qualified under MLI Select Tier 100 on a 5-unit project in March 2026. His architect had drawn two interconnected buildings sharing a party-wall on a single title — an architectural answer that worked under earlier readings of the rule. In May, CMHC issued a clarification on the “single building under single title” requirement that excluded that exact configuration. The deal lost Tier eligibility overnight. He found out from his broker, not from his lender, three weeks after the bulletin landed.

CMHC’s MLI Select program, with rules updated in February 2025, requires a minimum of 5 residential units within a single building under a single title to access the Tier-scored insurance product. Tier 100 unlocks 95% loan-to-cost (LTC), 50-year amortization, and reduced insurance premiums. Tier qualification itself is scored against three criteria — affordability commitment depth, accessibility unit count, and climate-impact measurement methodology — with the final tier (50, 80, or 100) determining the loan terms.

The February 2025 rule clarification narrowed several configurations that earlier underwriting had accepted, including some interconnected-building and split-title designs that brokers had been routing through Tier 100 since the program’s inception.

The cost of misreading the rule is enormous. One firm operating in a comparable Alberta market reported $35-40M of deals jeopardized and roughly $50M of stranded land deposits from the early-2025 rule changes, per MPA Magazine’s Q1 2026 multi-family lender pipeline survey. Losing MLI Select eligibility on a deal underwritten at 95% LTC and 50-year amortization typically collapses project-level IRR by 4-7 percentage points.

The GP’s options at that point are narrow: re-equity-call the LPs (which introduces both friction and timing risk), restructure the architecture to fit the corrected rule (which adds design fees and a re-stamp), or kill the deal entirely. None of those are decisions to make in the 30 days between permit submission and close.

The question to the lender is direct: “Given the February 2025 clarification, walk me through every assumption in your underwriting that depends on my configuration qualifying.” If the lender cannot answer that question against the current bulletin set in under 24 hours, the GP is not getting underwriting clarity — they are getting marketing.

Eligibility is the first gate. The second is whether the rate the lender quoted in spring still holds in summer.

2. Will you hold this rate through permit issuance + closing?

An Auburn Bay GP got a 4.18% pre-quote on a 5-year fixed in March 2026. The lender’s standard rate-hold was 90 days. By June, with permit issuance delayed by the R-CG-repeal council debate stretching into a second contested cycle, his rate had rolled to 4.42%. On a $7.5M loan, the 24 basis-point delta is roughly $18,000 of additional debt service per year. At a 6.5% capitalization rate, that one un-asked question erodes approximately $277,000 of stabilized value — money that no longer exists in his LP distribution model.

Calgary 5-year fixed multi-family debt rates ranged 4.04-4.29% in Q2 2026 per CBRE’s capital markets reporting, with MLI Select Tier 100 product typically sitting at the lower end of that band. Lender rate-holds for Calgary multi-family typically run 60-120 days, with some MLI Select underwritten quotes extending to 150 days at a slight basis-point premium.

LendCity’s Q2 2026 rate sheet places the standard hold at 90 days for conventional CMHC multi-family and 120 days for fully-underwritten MLI Select files. Beyond the rate-hold window, the lender is free to re-price against current market, which in a volatile rate environment can move 20-40 bp in a single month.

The math of a rate slip is unforgiving. A 24-25 bp move on a $7.5M loan adds roughly $18,000 per year in debt service. Compound that across a 5-year fixed term, and the lifetime cost of the slip is $90,000 — before considering the impact on the refinance valuation at term-end. At a 6.5% cap rate, the same $18,000 of additional annual debt service erodes $277,000 of stabilized value at exit. That is roughly the cost of two parking stalls, a partial elevator upgrade, or the entire landscape budget on a 6-unit infill build.

The question to the lender is specific: “If permit issuance is delayed past your standard rate-hold window, what is the cost — in basis points — to extend the hold by 30, 60, or 90 days?” The GP who has that number in writing before submitting the permit knows their downside. The one who doesn’t is exposed to the lender’s pricing committee on the worst day of the quarter.

Rate-hold protects one variable. Underwriting timeline protects the other — the calendar itself.

3. What’s your current MLI Select underwriting cycle, in calendar weeks?

A first-time multi-family GP in Discovery Ridge submitted an MLI Select Tier-scored package in April 2026 expecting an 8-week underwriting cycle based on his broker’s verbal estimate. The lender’s actual queue was running at 11 weeks. The deal closed mid-July instead of late May. Two months of additional land carry on a $1.8M land deposit at prime + 200 basis points cost roughly $30,000 in carrying cost that no LP had subscribed to absorb. The GP funded it personally to keep the LPs whole on their distributions — a decision that worked, but only because he had personal liquidity. Many first-time GPs do not.

CMHC MLI Select underwriting timelines run 6-12 calendar weeks depending on Tier complexity, lender pipeline depth, and the quality of the submitted package. Conventional CMHC multi-family (without MLI Select Tier scoring) runs 4-8 weeks. The variance is driven by three factors: climate-impact documentation completeness, sponsor financial-statement quality, and the depth of the lender’s pipeline at submission time.

Q2 2026 lender pipelines in Western Canada are running deeper than the prior year per the MPA Magazine 2026 Q1 multi-family lender pipeline survey, which means even well-prepared packages are queuing longer than the historical 6-8 week average.

Bridge or interim financing during an underwriting wait typically prices at prime + 200-400 basis points (a 9.45-11.45% range in Q2 2026) on shorter tenors, per CBRE Calgary Q2 2026 capital markets data. Every week of slip translates to roughly $2,500-$5,000 of carry on a $1.5M land position. Across a 4-6 week underwriting delay, the carrying cost differential between a confidently-quoted bridge facility and a panic-bridge taken at week 9 can run $20,000-$40,000. That money comes out of the GP’s promote — or out of the LP distribution, depending on the operating agreement.

The question to the lender is concrete: “What is your current MLI Select underwriting queue, measured in calendar weeks from submission to commitment? And what is the bridge facility you would write if I needed to land before commitment?” The GP who walks out of that meeting with a calendar in weeks and a bridge facility pre-quoted controls their timeline. The one who walks out with “we’ll see how the queue looks” is on the lender’s schedule, not their own.

The lender’s queue is one timing variable. The appraiser’s bias is another.

4. Which appraiser are you sending — and what comps are they using?

A Springbank-edge multi-family GP in 2026 had the lender’s appointed appraiser inspect a 6-unit project. The appraiser pulled comps from 2024 — pre-R-CG-launch — when the inner-city 4-plex market had been trading at a 6.2% stabilized cap rate. By 2026, post-R-CG-repeal vote, comparable 4-plex resale activity was trading at 6.5-7.0%. The 30-50 basis-point cap-rate swing reduced appraised value by 8-12%, knocked the loan-to-value down by the same margin, and triggered an additional $300,000 equity call to close. The GP raised it — barely — by extending the subscription window and personally back-stopping a soft commitment that wavered. None of that needed to happen.

Calgary inner-city multi-family cap rates ranged 5-7% in Q2 2026 per CBRE Calgary’s Q2 2026 multi-family report, with Class C and value-add product at the higher end of the band and Class A purpose-built rentals at the lower end. Cushman & Wakefield’s Calgary Q1 2026 multi-family report reinforces the split: completed Class A product compressed mildly post-R-CG-vote on supply-scarcity perception, while value-add and infill new-construction inputs absorbed regulatory uncertainty into their discount rate. The result is a bifurcated comp set — one half pre-repeal-vote and one half post-repeal-vote — and the appraiser who pulls only one half is reading half the market.

The pre-R-CG vs post-R-CG cap-rate environment is genuinely split, and that split has real consequences for the underwritten loan amount. The April 8, 2026 council vote (12-3 in favour of repeal, effective August 4, 2026) increased perceived supply scarcity for as-of-right multi-family on infill lots — slightly compressing cap rates on completed product — but also injected regulatory uncertainty into new development underwriting, slightly expanding cap rates on under-construction or paper-only deals per the HCM Calgary 2026 multi-family brief. An appraiser pulling exclusively pre-vote comps from a Class A purpose-built resale is reading a different market than the one the GP is actually building into.

The question to the lender is pointed: “Which appraiser are you sending? Can I see their last three Calgary multi-family appraisals — and what comp date-window are they currently working from?” The GP who challenges the comp set before the report goes in — providing a six-comp package that brackets pre- and post-vote transactions, with weighting commentary — protects six figures of underwriting margin. The one who waits to see the appraisal lands on the lender’s number is reading the final answer.

And once the appraisal is in, the lender’s covenants are what determine whether the deal survives — or whether the next decision becomes the trigger event.

5. What covenants — DSCR, NOI hurdle, lease-up — am I signing into?

A Cranston-edge GP in 2026 signed an MLI Select loan with a 1.20x DSCR (debt-service coverage ratio) hurdle at year 1 stabilization and a 90% lease-up covenant by month 18. The lease-up market softened in Q2 2026 as new supply from the post-R-CG-vote permit pipeline hit the rental market simultaneously across several Calgary submarkets. At month 17, his lease-up was at 82%. The lender’s monitoring team noticed. A covenant-cure conversation started — the kind of conversation that has only three outcomes, all of them moving the GP’s IRR in the wrong direction.

MLI Select loans typically carry a 1.10-1.20x DSCR covenant at stabilization, lease-up hurdles in the 85-90% range by months 12-18, and occupancy/rental-rate triggers tied to the original underwriting assumptions, per the CMHC MLI Select Underwriting Guide. The DSCR test is the most-cited covenant breach in multi-family workouts. A 5% miss on rental-rate or a 7-10% lease-up shortfall is usually enough to drop a 1.20x underwritten DSCR to 1.05x — into covenant-breach territory — particularly on a 95% LTC Tier 100 deal where there is no equity cushion to absorb the variance.

A covenant cure typically takes one of three forms, per MPA’s 2026 multi-family workout case studies. The first is additional equity injection from the GP and LP pool — usually 3-7% of the loan amount, raised in 60-90 days, often during a market window the GP did not plan around. The second is modified amortization, which the lender may offer if the operating fundamentals are improving but lease-up is slow; this extends the term but does not change the principal. The third is forced refinance, which at current rate environments means converting a 4.04-4.29% MLI Select loan to a conventional 5.5-6.5% mortgage — a 150-200 bp re-pricing that destroys the original deal economics.

The question to the lender is unambiguous: “Walk me through every covenant, every trigger threshold, every cure mechanism, and every notice period. What is the margin between my underwriting assumptions and the trigger?” The GP who has that table in front of them before signing closes a deal they can defend. The one who finds out about the 90% lease-up covenant at month 17 is having the covenant-cure conversation, not running it.

Covenants govern the back end. The front end — the equity stack — is where the next question lives.

6. How will the equity stack look if I lose one tier of MLI Select scoring?

A Mahogany GP underwrote a Tier 100 MLI Select deal at 95% LTC on a $9M project. The deal modeled clean at Tier 100. In due diligence, the climate-impact scoring landed differently than the broker’s verbal — the deal scored Tier 80 instead, dropping LTC to 90%. The 5% equity delta on a $9M deal is $450,000 of additional LP equity to raise. The GP had six weeks between the Tier-scoring confirmation and closing to source it — between subscription agreements being countersigned, KYC running, and the wire dates landing. The deal closed, but only because two existing LPs over-subscribed at the last moment to back-stop the gap. Most GPs do not have that LP roster on speed-dial.

MLI Select tiers scale loan-to-cost from 85% (Tier 50) to 95% (Tier 100), and amortization from standard CMHC terms to 50 years for the highest tier. The scoring is sensitive to three criteria, but climate-impact scoring is consistently the most underwriting-sensitive of the three, per CMHC’s Climate-Impact Scoring Bulletin 2025. Small specification changes can swing the climate score 5-15 points: envelope U-value (the building shell’s thermal performance), mechanical system selection (heat pump vs gas, balanced ventilation), and embodied carbon disclosure methodology (cradle-to-gate vs cradle-to-grave, third-party verified vs sponsor-stated).

The interaction with LEED v5 is now material to underwriting. The CAGBC opened LEED v5 registration on April 28, 2026 (one year after USGBC’s April 28, 2025 release), and the new version’s emphasis on equity, decarbonization, and quality-of-life metrics aligns increasingly with MLI Select’s climate-impact scoring methodology. Up to 6 Materials & Resources points are available under LEED v5, with an “Optimized Product” requiring at least a 20% global-warming-potential (GWP) reduction plus at least a 5% improvement in two other impact categories.

The GPs who plan for LEED v5 certification from design onward are also the ones reliably hitting Tier 100 climate-impact scores. The ones treating LEED as an afterthought are landing in Tier 80 — and discovering the equity gap six weeks before close.

The question to the lender is hard-edged: “Show me the equity stack at every Tier outcome — 50, 80, and 100. What pre-circled LP capital do I need to have committed for the downside scenarios?” The GP who models all three Tier outcomes and pre-circles capital for Tier 80 closes calmly even when scoring lands lower than verbal. The one who only models Tier 100 is running a single-scenario plan against a multi-scenario underwriting committee.

Equity sources flex one way. The lender’s own deposit and CMHC application timing flex the other.

7. When do you need full CMHC application and what triggers a deposit?

A Hillhurst GP submitted a building permit application in mid-June 2026 with a closing target of late September. The lender’s internal calendar required the full CMHC MLI Select application package by July 15 to close in late September — a date the GP’s broker had mentioned in passing but never written into a Gantt. The GP’s architect was still finalizing the climate-impact narrative in early July. By July 14, the application went in incomplete. CMHC deferred the file for missing documentation. The September close slipped to November. Two months of land carry on a $1.4M position, plus an LP renegotiation as the close-date shifted past the original subscription window, plus an updated rate environment when the file re-queued.

CMHC MLI Select applications require complete underwriting packages — sponsor financial statements (audited or review-engagement quality), full project pro forma (sources and uses, operating assumptions, sensitivity tables), climate-impact scoring documentation (with third-party certification where claimed), and explicit accessibility and affordability commitments (signed and binding). These packages are submitted by deadlines that lenders set against their own underwriting calendar, not against CMHC’s. Deposits typically range 0.5-1.0% of the insured loan amount, paid at full application submission, and are non-refundable in most circumstances. On a $7M loan, the deposit ranges from $35,000 to $70,000.

The most-cited cause of MLI Select application delay is incomplete climate-impact documentation — particularly the LEED v5 or equivalent third-party certification that supports the highest-tier climate points. The CAGBC LEED v5 transition brief makes the timeline explicit: a project pursuing LEED v5 certification needs the design-phase documentation pinned six to eight weeks before the CMHC application date, which means the lender’s application calendar effectively dictates the architect’s deliverable schedule from the moment the GP signs the engagement letter. GPs working backward from a target close date should plan the climate documentation deliverable 16-20 weeks before close — not 8.

The question to the lender is operational: “Give me your CMHC application calendar, working backward from my target close. What documentation triggers your deposit ask? What is the consequence of a late deposit or an incomplete application?” The GP who walks into the lender’s office with that calendar in hand controls the close. The one who waits for the lender to push controls nothing.

Seven questions, one underwriting calendar, one rate environment. The GP who asks them in June closes in September. The one who doesn’t, closes in November — or doesn’t close at all.

FAQ

Q1: What is the MLI Select unit-count requirement after the February 2025 rule update?

CMHC’s MLI Select program (rules updated February 2025) requires a minimum of 5 residential units within a single building under a single title to access the Tier-scored insurance product. Tier 100 unlocks 95% loan-to-cost, 50-year amortization, and reduced premiums. Earlier interpretations of multi-building or split-title configurations were narrowed in the Feb 2025 clarification, and several deals that brokers had been routing through Tier 100 under earlier readings have since been re-tiered.

Q2: What are typical Calgary 5-year fixed multi-family debt rates in Q2 2026?

Calgary 5-year fixed multi-family debt rates ranged 4.04-4.29% in Q2 2026 per CBRE’s capital markets reporting, with MLI Select Tier 100 product typically at the lower end of that band. Bridge or interim financing prices at prime plus 200-400 basis points. The rate environment is sensitive to Bank of Canada policy moves and to CMHC insurance-premium adjustments, both of which can move the all-in cost of capital 20-40 bp in a single quarter.

Q3: How long does CMHC MLI Select underwriting take?

CMHC MLI Select underwriting timelines run 6-12 calendar weeks depending on Tier complexity, the lender’s pipeline depth at submission time, and the quality of the submitted package. Conventional CMHC multi-family insurance (without Tier scoring) runs 4-8 weeks. Climate-impact documentation completeness is the most common source of underwriting delay, particularly when the project pursues LEED v5 certification as part of its Tier 100 scoring strategy.

Q4: What is the typical MLI Select DSCR covenant?

MLI Select loans typically carry a 1.10-1.20x debt-service coverage ratio (DSCR) covenant at stabilization, alongside lease-up hurdles (often 85-90% by months 12-18) and occupancy/rental-rate triggers tied to the original underwriting assumptions. Covenant cure events typically require additional equity injection, modified amortization, or forced refinance — each of which moves the GP’s IRR in the wrong direction. The DSCR test is the most-cited covenant breach in Calgary multi-family workouts.

Q5: How does the August 4, 2026 R-CG repeal affect multi-family lender underwriting?

The April 8, 2026 Council vote to repeal R-CG (effective August 4, 2026) injects regulatory uncertainty into Calgary multi-family underwriting on parcels affected by the reversion. Lenders may require updated zoning confirmation, re-stamped engineering for changed unit counts, and updated appraisals reflecting post-repeal market comps. The cap-rate environment is bifurcated — pre-vote comps versus post-vote comps — and the appraiser’s comp window directly affects the loan-to-value math.

Q6: What deposit does a CMHC MLI Select application require?

CMHC MLI Select application deposits typically range 0.5-1.0% of the insured loan amount, paid at full application submission. The deposit is non-refundable in most circumstances and is structured to recover CMHC’s underwriting effort regardless of whether the deal ultimately closes. Specific terms vary by approved lender, and some lenders charge an additional commitment fee separate from the CMHC deposit. On a $7M loan, total upfront fees can range from $35,000 to $90,000.

Sources

- CMHC MLI Select Product Guide (February 2025) — https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/multi-unit-insurance/mli-select

- CMHC MLI Select Underwriting Guide — https://www.cmhc-schl.gc.ca

- CMHC Climate-Impact Scoring Bulletin 2025 — https://www.cmhc-schl.gc.ca

- CBRE Calgary Q2 2026 multi-family capital markets report — https://www.cbre.ca

- Cushman & Wakefield Calgary Q1 2026 multi-family report — https://www.cushmanwakefield.com/en/canada

- MPA Magazine — 2026 Q1 multi-family lender pipeline survey — https://www.mpamag.com

- City of Calgary — Rezoning project page — https://www.calgary.ca/planning/projects/rezoning.html

- LendCity — 2026 Q2 multi-family rate sheet and application checklist — https://lendcity.ca

- CAGBC — LEED v5 transition brief — https://www.cagbc.org

- HCM Calgary — 2026 multi-family brief — https://hcmcalgary.ca

About Omega Group

Omega Group is the Calgary umbrella for three concrete brands serving Western Canadian multi-family developers, custom builders, and infrastructure contractors: Omega 2000 Cribbing (foundations, since 1988), Omega Ready Mix (volumetric ready-mix), and Omega Precast (insulated and architectural precast). The Group’s editorial voice speaks from inside Calgary’s construction calendar — not from the lender side of the table.